MIT Golub Center for Finance and Policy

Economics

Why Today’s Inflation Is a Fiscal and Credit Policy Hangover

This blog post is based on a talk presented at the Shadow Open Market Committee on February 11, 2022.

Whether the recent burst of inflation is likely to be transitory or persistent is a question much on peoples’ minds, as is what the Fed should do about it. I want to emphasize the importance of fiscal and credit policies for several reasons:

First: These policies likely had, and are still having, an enormous impact on aggregate demand and on household and firm savings.

Second: Credit policies are an important driver of inflation that often go unrecognized. They have become an ever more frequently used policy lever, but their macroeconomic impacts and costs continue to be seriously mismeasured.

Third: The overhang of those policies has caused many observers to wrongly attribute the recent surge in inflation to mistakes in monetary policy. There is general agreement, and I concur, that the Fed needs to start taking more aggressive action to counter inflationary expectations. However, it is not clear whether the Fed should have acted more quickly to tighten and try to head off inflation, or whether doing so would have reduced the largely policy-induced inflationary surge we’re now experiencing. Earlier action by the Fed may very well have been the wrong call.

Milton Friedman famously said that inflation is always and everywhere a monetary phenomenon. While that is probably true, the money need not come from a monetary authority. Instead, it can come from fiscal and credit policies. The mechanisms that lead from a helicopter drop of money on the populace should be much the same whatever the source of the funds.

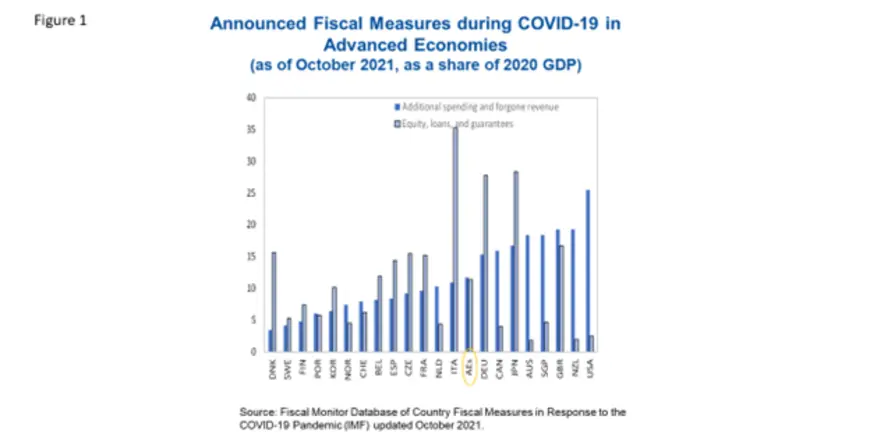

The sharp drop-off in economic activity triggered by the pandemic was met by a massive fiscal response by governments throughout the developed world. Chart 1 from the IMF highlights the unprecedented size of traditional fiscal actions, such as the increased spending through expanded unemployment benefits and tax cuts. At about 25% of GDP by the IMF’s calculations, the US topped the international charts for aggressive fiscal policy as a percentage of GDP, followed by Great Britain, Australia, Singapore, Canada, New Zealand, Germany and Japan, all of which devoted more than 15% of GDP to new fiscal measures.

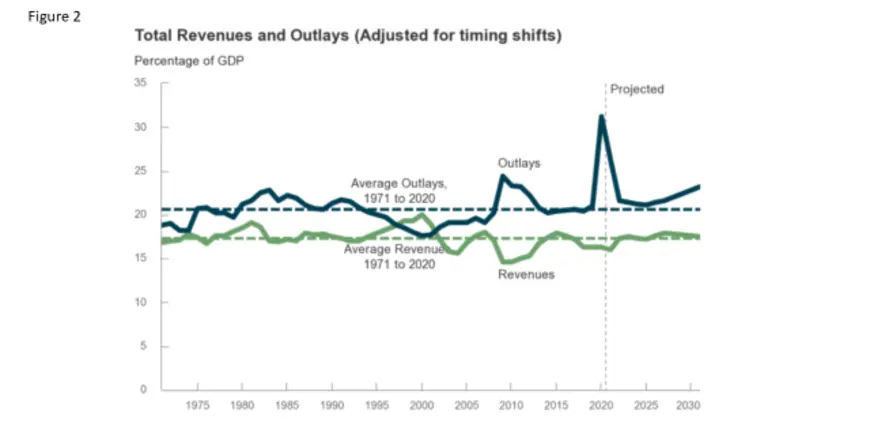

Looking more directly at the magnitudes for the United States, the sum of 2020 and 2021 budget deficits totaled about $6 trillion, 15% of GDP in 2020 and 12.4% of GDP in 2021, according to the Congressional Budget Office (see Figure 2). That unprecedented level of spending was largely accommodated by Fed purchases of Treasury securities, but the mechanism that moved money from the government to households was fundamentally fiscal.

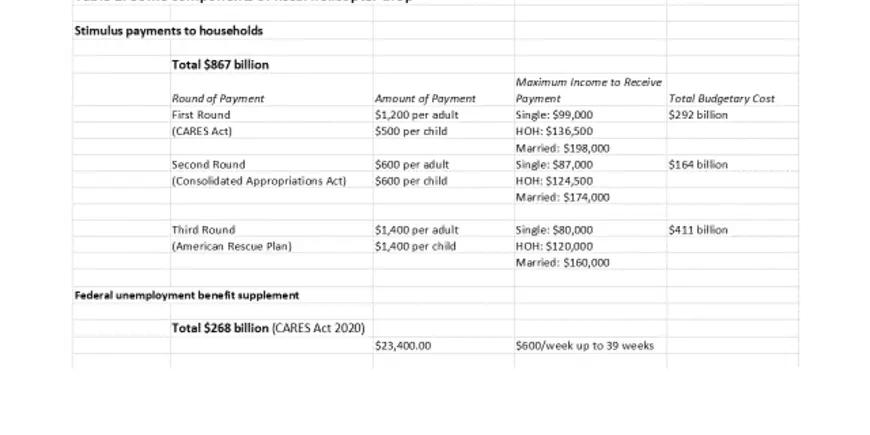

Table 1 highlights the three rounds of stimulus to households that were most obviously equivalent to a large helicopter drop of money.[1] Supplemental federal unemployment benefits are included because to the extent that they more than replaced income for some households, the incremental amounts were like a helicopter drop.

Turning back to Figure 1 from the IMF, it highlights the massive amount of public funds that were made available in the form of credit assistance, which was primarily in the form of loan guarantees and direct government loans to small businesses, households and corporations. In terms of the notional amounts made available, in some places like Italy that imposed a broad debt repayment moratorium, credit support dwarfed traditional fiscal measures. Overall for the countries in this chart, the average envelope of available credit assistance equaled the amount of traditional credit assistance, with each totaling about 10% of 2020 GDP.

Credit policy is fundamentally fiscal when it involves legislative or executive action—the typical structure being a Treasury set-aside to absorb default losses on subsidized loans. However, the channel through which credit policy stimulates the economy and potentially leads to inflation is quite similar to that of monetary policy. Lowering interest costs and fees motivates additional borrowing and spending. That increases aggregate demand, eventually putting upward pressure on prices.

Credit policy can be more powerful than monetary policy, and I think this was the case during the pandemic. Importantly, credit policies significantly reduced credit rationing in a way that monetary policy cannot, by incentivizing banks to make loans to businesses and households that otherwise would have been deemed too risky to lend to.[2]

Most significantly in the U.S., the Paycheck Protection Program effectively provided an $800 billion cash helicopter drop on businesses because the loans were forgivable. The U.S. relies on ongoing federal credit programs much more than most other countries, and has a particularly large footprint in residential mortgages and student loans. That allowed the U.S. to provide large-scale credit relief to households through forbearance on government- backed mortgages from Fannie Mae, Freddie Mac, FHA and VA, and on a moratorium on federal student loan debt repayment or collection actions.

How much money did mortgage forbearance put in people’s pockets? It’s been reported that 2.1 million mortgages, representing $417 billion in unpaid principal balance, went into forbearance for a period that initially was set at six months but was subsequently extended to over a year. A rough calculation suggests households whose mortgages were in forbearance reduced their mortgage payments by about $12,000 annually on average. Although the loans will ultimately have to be repaid, the unpaid amounts will not come due until the final payment date. These policies did not generate much wealth, but they did provide considerable cash-in-hand that wouldn’t otherwise have been available.

A similar story can be told for student loans, where there was a payment moratorium on about $1.5 trillion in federally-held student loans, representing 4.34 million borrowers. A rough estimate suggests that the annual cash saving per loan is about $4,100.

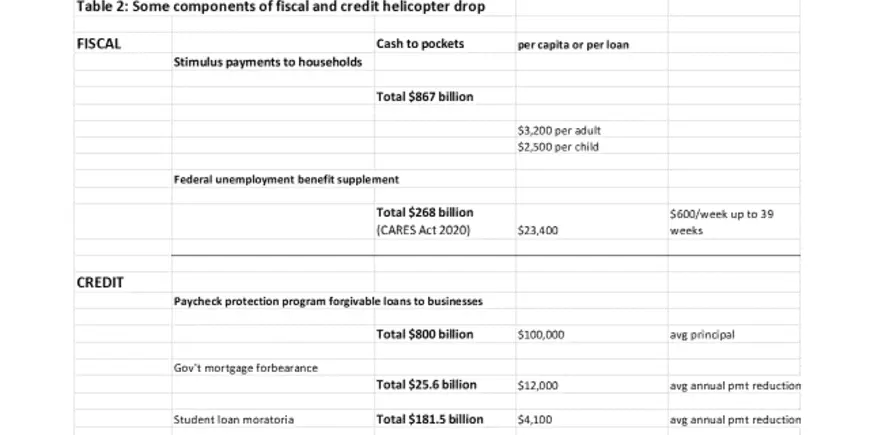

What is important about these credit forbearance actions is that they collectively put more than $200 billion of cash into people’s pockets that they didn’t expect to have. That $200 billion contributes nothing to the reported budget deficit. Table 2 summarizes these calculations, and shows that the magnitude of helicopter-like cash arising from credit actions was similar to the amounts from more traditional fiscal policies.

I want to make clear that for many of those who had lost jobs or business income, these cash infusions were a lifeline, not a windfall. And I strongly support the idea that the government can play a uniquely useful role in providing insurance against catastrophic events, which is effectively is what much of this assistance was intended to do.

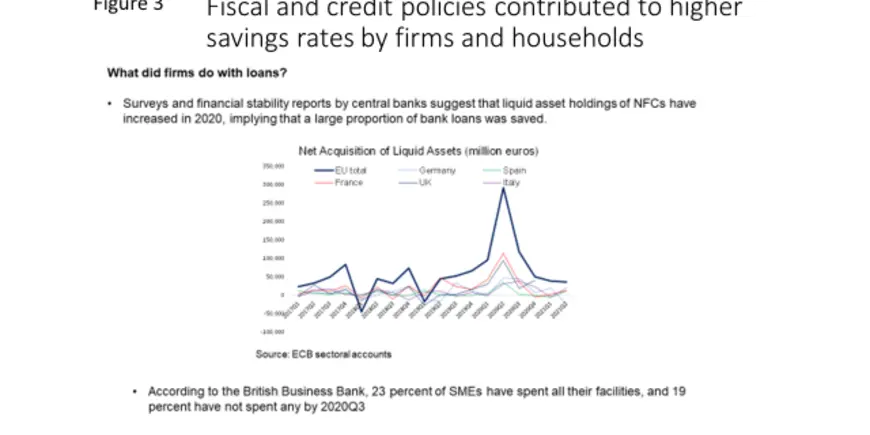

However, because of programs like the Paycheck Protection Program where the funds were loosely targeted, for a substantial number of households and businesses these policies created a windfall—a helicopter drop of cash. Because it was a windfall and spending opportunities were constrained, much of that money was saved rather than spent (Figure 3), setting up the conditions for a protracted period of higher demand once pandemic restrictions were lifted.

What does this all mean for monetary policy? I’ve made the case that it was expansive fiscal and credit policy, rather than easy monetary policy, that dropped large amounts of cash on individuals and businesses. In fact, businesses were reluctant to borrow through traditional bank and capital market channels, and small changes in base interest rates wouldn’t have changed that—it was a highly risky period and not the time to make major investments. Had the Fed tightened, the demand created by fiscal and credit policies would have still been there. And it is doubtful it would have made sense, economically or politically, for the Fed to try to undo deliberate emergency fiscal actions until the crisis period had ended. The Fed is figuring out how to do that now, and I think it is appropriate to withhold judgment for a while longer.

Charts and Tables

-

Figure 1