How retirement saving incentives amplify wealth gaps in the U.S.

Changing how more than $300 billion of annual incentives are allocated could close the racial gap in retirement savings by a third, a new study finds.

At an average match of 50 cents per dollar contributed, a tax-favored employer-sponsored account such as a 401(k) or 403(b) is one of the best investment opportunities available to save for retirement.

But the system rewards those who can set aside more of their income — providing them with generous tax benefits and employer contributions — while putting people who can’t afford to save as much at a disadvantage, new research shows.

The average rate of contribution by Black and Hispanic workers to employer-sponsored retirement plans is roughly 40% lower than that of white workers, according to the working paper “Who Benefits From Retirement Saving Incentives in the U.S.? Evidence on Racial Gaps in Retirement Wealth Accumulation.”

“We know that Black and Hispanic workers in the U.S. typically are going to be entering their careers and living their lives in a position with fewer liquid resources available,” saidone of the paper’s authors and an assistant professor of finance at MIT Sloan.

Because there are tax penalties for taking out retirement money early, Black and Hispanic workers often face a dilemma: “Do I save for retirement, or do I save to help protect myself against a rainy day?” Schmidt said.

Broadly popular programs

In the U.S., there are two large institutional supports for retirement savings. One is employers, which usually match employees’ contributions. The second is the government, which allows workers to defer taxes on their contributions until they withdraw funds, which goes a long way toward wealth accumulation.

The average rate of contribution by Black and Hispanic workers to employer-sponsored retirement plans is roughly 40% lower than that of white workers.

Both programs are broadly popular in the U.S. Employers contribute around $190 billion a year in the form of matching contributions; tax incentives offered by the government are worth around $120 billion a year, Schmidt said.

“In terms of helping people build wealth, retirement accounts are unique from the perspective of getting massive support from employers, massive support from the government, and benefiting from compound interest through stock appreciation,” said another of the paper’s co-authors and an assistant professor at MIT Sloan.

Schmidt, Choukhmane, and co-authors Jorge Colmenares, Cormac O’Dea, and Jonathan Rothbaum set out to better understand the extent to which retirement accounts and the strong incentives attached to them might exacerbate existing wealth inequality that has persisted for decades.

“When we study retirement, there’s been a lot of interest in whether these tax subsidies work and increase saving but a lot less on how those benefits are distributed,” Choukhmane said. Given how much money is at stake, it’s important to know how retirement incentives contribute to inequality. “Being able to systematically document how it’s distributed and who’s getting left out from this system was a question that really interested us,” he said. “It was really at the intersection of our interests.”

The authors created a dataset containing the following information:

- Administrative data on Americans’ retirement saving behaviors (using W-2 tax forms).

- Race and ethnicity demographics of a large sample of U.S. employees (using data from the U.S. Census Bureau).

- Details on employer-sponsored retirement plans (using Form 5500, a tax form companies file that contains information on their retirement plan offerings).

Having this information allowed the authors to see both how employers’ matching incentives were distributed and how people responded to them. It also showed how a person’s saving behaviors correlated with factors such as the income of their parents, their marital status, whether they had children, and if they were a single parent.

The baseline sample included 12.48 million individuals ranging from age 24 to 59 ½ who participated in the 2008 – 2017 American Community Surveys.

Here are some of the researchers’ findings:

If your parents are richer, you're going to save more

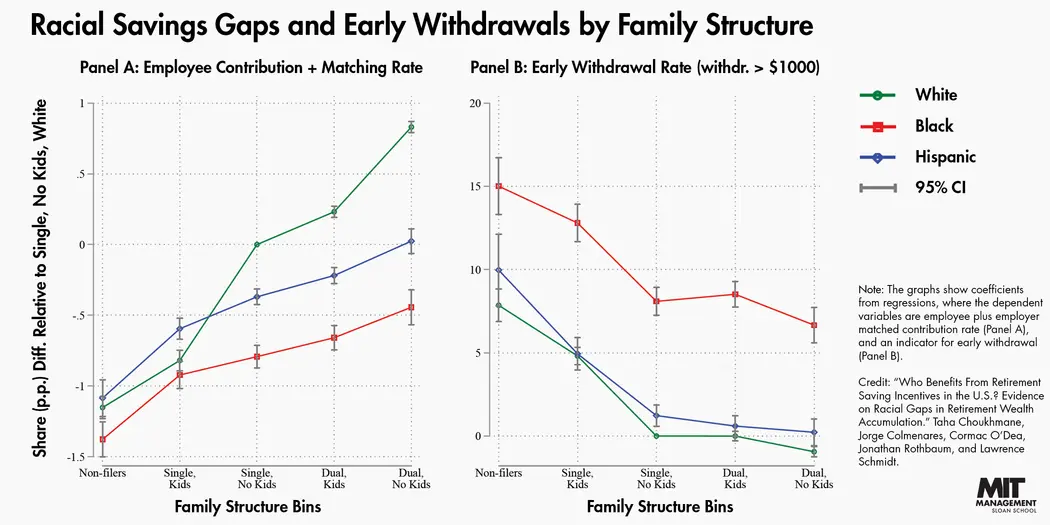

Earned income isn’t the only factor that determines how much a person puts toward retirement. The authors found that a person’s family structure plays a role in inequality by giving people from wealthy backgrounds an edge. They arrived at this conclusion by tracing the link between parents and their children from tax records (via a parent claiming a child as a dependent, then tracking the child as they went on to have financial independence).

“What we find is a strong effect of your parental income and family background on your own savings,” Choukhmane said. “Everything else being the same, if two people work at the same firm in the same occupation and make the same income — if your parents or your spouse is richer, you’re going to save more.”

Conversely, "If you are a single parent, you will save less than your married co-workers and receive less in tax and employer subsidies for retirement saving,” Schmidt said.

This can cause a chain reaction, where wealth inequality persists for a long time. “It becomes really hard for those who start with less to escape. Because they cannot afford to save, they don’t get the subsidies, which means that the next generation is also going to face the same type of hardship,” Choukhmane said.

In contrast, those who begin their careers in a more secure financial position benefit from extremely high rates of return as a result of these subsidies. Without policies to address wealth inequality, this pattern can persist for generations, Choukhmane said.

Black Americans are more likely to withdraw funds early

In an indication that they have less of a financial cushion elsewhere, the research found that Black Americans are twice as likely as white workers to take money out of their retirement accounts early; Hispanics are 21% more likely to withdraw early.

Withdrawing money early usually involves paying income tax and a one-time 10% tax penalty. So Black and Hispanic Americans are not only getting fewer tax benefits on the savings side — they’re also paying more in taxes when they take these withdrawals.

“Here, again, we found really large disparities across racial and ethnic groups,” Choukhmane said. “If you’re willing to pay those tax penalties and take money from your retirement account, it’s telling us that you don’t have money just sitting around in your checking account to use or [that a] parent could give you some money to deal with an emergency.”

When sorting by parental income, the researchers also found large gaps in the propensity to take early withdrawals, which echoed earlier findings.

How do these tax benefits for saving and penalties on early withdrawals translate into missed savings? For every dollar of tax benefit that a white American receives, the average Hispanic American gets 62 cents, or 38% less. For Black employees, it’s 31 cents, which is 69% less. Taking an early withdrawal on their retirement account contributes greatly to these disparities and diminishes the extent to which Black and Hispanic savers benefit from tax benefits, the researchers said.

One solution: Distribute benefits more equitably

One question that emerged from the researchers’ discovery that there is a wide range in how much employers match was, what if employers were to put the same number of dollars they were planning on allocating for total retirement funds into everyone’s accounts uniformly instead?

“Suppose that instead of tying the employer subsidy to my own savings rate or tying the tax benefit to my own savings rate, what if instead we just allocated that uniformly proportional income?” Schmidt said.

“If we can just take the money the government is already spending, make simple changes to the formulas that the government encourages employers to adopt, or change the tax code, you could reallocate a lot of that money in a way that would lead to more equitable outcomes,” Choukhmane said.

Doing so could close the racial wealth gap by 30%, their research estimates, and wouldn’t involve new expenses for employers or the government. Schmidt acknowledged, however, that that might make people less willing to plan for retirement using their own resources.

Also needed: More flexibility in retirement plans

The authors’ research showed that people are less likely to save if their household demand for liquidity is high: Employees who are short on cash are reluctant to contribute to a retirement fund, knowing they’ll be penalized if they need to withdraw money in an emergency.

“Our findings suggest that there can actually be a deterrent effect in making these accounts illiquid,” Schmidt said. The penalty was intended to keep people from spending their retirement money on other things, but an unintended consequence is that it might make retirement accounts less desirable and reduce participation in the first place.

Related Articles

A new law that was recently passed, called Secure 2.0, expanded the situations when savers can take penalty-free distributions to include disaster relief, terminal illness, or other personal or family emergency expenses. Some provisions are in place now, while others will become effective later this year. For example, as of this year, people can take an emergency distribution of up to $1,000 once every three years.

“So there’s a new opportunity now to have these accounts be a little bit more liquid, Schmidt said, “and that might actually be particularly helpful for Black and Hispanic Americans who tend to have lower liquid resources to begin with.”

While this is useful progress, workers will continue to face hefty tax penalties when tapping into their retirement account after a job loss or a family member’s health emergency. These new provisions might, therefore, not be enough to get those who have little saved for an emergency to participate in retirement accounts, Schmidt said.

The power of guidance from the government

More broadly, Schmidt and Choukhmane were surprised to see such a big range on employers’ matching incentives (even for two people who worked in the same industry), “which maybe reflects the fact that employers aren’t sure what the best policy is,” Schmidt said.

He said that the government identifies certain types of accepted formulas in safe harbor plans, which exempt employers from a complex annual nondiscrimination test in 401(k) plans.

Around 40% of employers choose to go with these plans, which suggests that in terms of allocating these employer-based subsidies, there’s a lot of opportunity for the government to wield soft power and strongly nudge companies to choose specific formulas.

“You don’t think of it as something that could have a significant impact on racial wealth inequality or intergenerational inequality in the U.S., but I really think that something as simple as that — changing what is a recommended safe harbor formula — could have large effects,” Choukhmane said.

Read next: Couples miss out when they fail to coordinate retirement benefits