New GCFP research showcases reverse mortgage market’s potential and challenges

Reverse mortgages are a financial innovation designed to help retirees free up the savings tied up in home equity without being forced to move. Access to those funds can make a big difference in the quality of life for house-rich, cash-poor, retirees. Yet the product has been slow to catch on. A new study by GCFP senior fellow Dr. Mark Warshawsky, “Retire on the House: The Use of Reverse Mortgages to Enhance Retirement Security,”takes an in-depth look at the reverse mortgage market and its potential for growth.

Dr. Warshawsky finds that:

- While retirement savings in the U.S. are very low for almost all except for the wealthiest older households, substantial savings in the form of home equity extend much further down the income distribution. Home equity is the only significant financial asset for many older households.

- Currently about 55% of households with head aged 62-74 appear eligible for a reverse mortgage. The eligible pool is found using a weak filter on affordability and data from the Health and Retirement Survey (HRS).

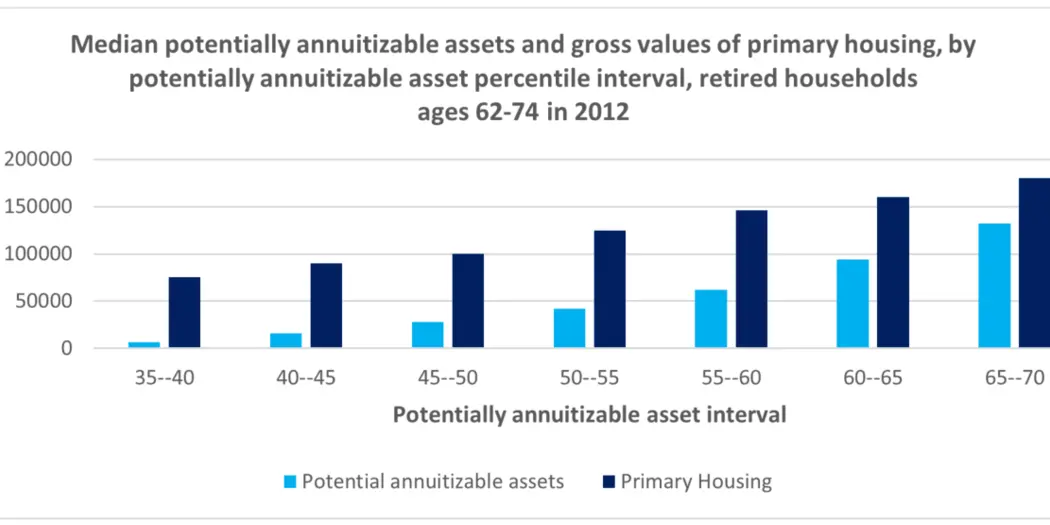

- Only about 12% of households, however, appear to be good candidates to use reverse mortgages to create an annuity to supplement income. This much smaller number is derived by applying tighter filters to HRS data that take into account the high costs of the current reverse mortgage offerings and other suitability assumptions. Potential demand would be higher if a lower cost product were to become available, or if the non-annuity uses of reverse mortgages were considered.

- Other countries have also introduced reverse mortgages. As in the U.S., to date the take-up rates have been low.

Median Potentially annuitizable assets and gross values of primary housing, by potentially annuitizable asset percentile interval, retired households ages 62-74 in 2012

Also included in the study is an extensive survey of the literature on reverse mortgages that is a must-read for researchers, regulators and practitioners who are interested in developing a deeper understanding of what is known about the product and its challenges.

Dr. Warshawsky’s study, which was commissioned by the GCFP, is the most recent contribution to the Center’s ongoing research agenda on reverse mortgages. An earlier study by GCFP Director Deborah Lucas, “Hacking Reverse Mortgages,” documents the high costs of the current government HECM program for borrowers and describes the structural problems in the HECM program that contribute to those costs. “The enormous footprint of government policy in all aspects of retirement finance, including reverse mortgages, make these issues central to our core mission of addressing issues at the intersection of finance and policy,” notes Lucas.

In the U.S., almost all reverse mortgages are issued under the government’s Home Equity Mortgage Conversion (HECM) program, which is run by the Federal Housing Administration. HECM loans are offered and administered by private lenders.

A reverse mortgage allows people over the age of 62 to borrow against the equity in their homes, with no obligation to repay the mortgage as long as they occupy the house. Mortgage interest and fees are rolled into the loan balance, which is only repaid after the borrower moves or dies. There is no recourse to the borrower beyond the value of the house—the borrower can forfeit the house if it is worth less than the loan balance. If the house is worth more than the loan balance, the borrowers or their heirs can repay the loan and keep the house.