7 principles for the ‘perfect portfolio’ from a top MIT economist

In a new book, six Nobel laureates and “Wall Street’s Wisest Man” share insights and investment advice on finding that perfect mix of risk and reward.

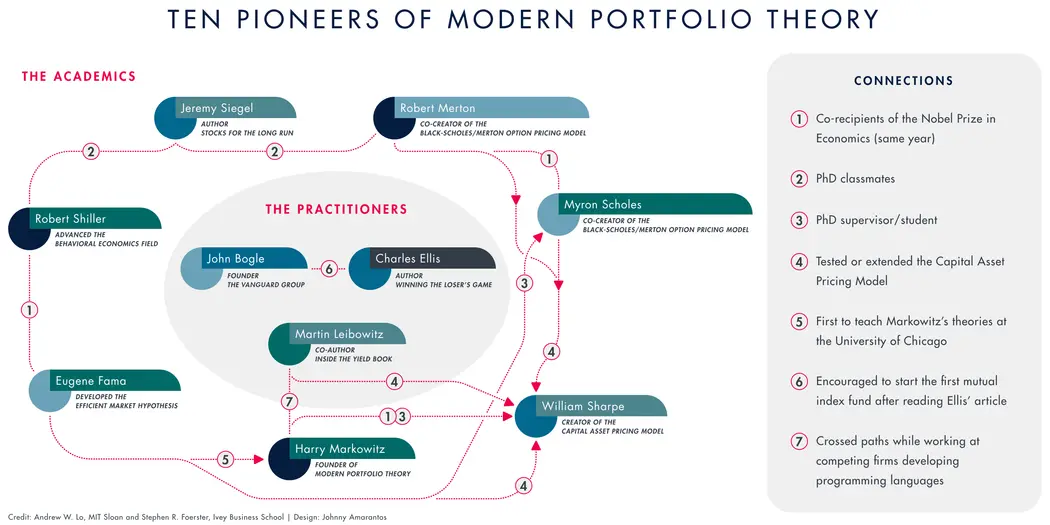

Imagine you’re in a room with six Nobel economists and Wall Street’s “wisest man” — what investment advice would you ask them?

While the odds of that meetup are slim, a new book from MIT Sloan professorand Ivey Business School’s Stephen R. Foerster offers a similar opportunity to look inside the minds of investment luminaries such as Myron Scholes,and Robert Shiller.

“In Pursuit of the Perfect Portfolio: The Stories, Voices, and Key Insights of the Pioneers Who Shaped the Way We Invest,” provides insights from 10 experts on topics including diversification, market timing, and the concept of a perfect portfolio and whether it’s possible to achieve that right mix of risk and reward.

“Our perfect portfolio today is really just a snapshot of what’s best for you at the moment and in the current environment,” the co-authors write. “The pursuit of the perfect portfolio is all about adapting to our current income, our spending habits, our financial goals, the environment, and expected returns.”

In the following excerpt, Lo and Foerster list their seven principles for constructing a perfect portfolio.

++++++

1

Determine how much expertise you have in financial planning and how much time and energy you’re willing to devote to managing your perfect portfolio. This will determine whether you can embark on your investment pursuit alone or whether and when you should seek professional help. In the same way that you may need to see an obstetrician, surgeon, or allergy specialist [for your physical health], you may also need to seek the assistance of financial specialists with expertise in mortgages, taxes, or estate planning.

2

Determine what your current and future financial needs are. This isn’t easy and requires deep personal reflection and a significant time commitment as well as regular reviews and some financial expertise, so you may also need the help of a professional here. Some obvious starting points are identifying your current income, both professionally and through any current investments. Next, identify your current expenses. The harder part is identifying future income and expenses. Don’t forget about Social Security and the important decision of when to take it. There may be some tough decisions involving family planning, saving for education, and retirement planning. The key is to start with overall life goals, then translate them into financial goals.

3

Find your comfort zone regarding financial gains and losses. How much can you lose in your savings or retirement account before you begin to freak out and start moving your assets into safer investments? How much will you allow your portfolio to grow before you decide that you want to lock in your gains? Think about the riskiness of your job or your business and what illiquid assets you might hold. Even if you can’t hedge against some risks, you don’t need to double down. For example, you may not want to invest in your own company (if it’s a publicly traded one), or even in companies in your industry. If recessions lead to big problems in your business, then a portfolio that might crash in recessions or becomes illiquid along with your job isn’t such a good idea.

4

Think about your investment philosophy and what you believe about markets. We hope that the journey with our investment pioneers has inspired you to reflect and develop your own philosophy. For example, are you in Eugene Fama’s camp, and are you convinced that, by and large, markets are efficient (particularly the U.S. stock market)? If so, then index funds are the place to start. That’s what the average investor would probably do. Do something else only if you think you’re different from the average. But also recognize, as Robert Shiller and other behavioralists point out, that almost everyone thinks they’re smarter than average. Be prepared to update your investment philosophy based on new and convincing evidence.

5

List all the assets that you have and the assets you’re willing to hold, such as mutual funds, exchange-traded funds, stocks, bonds, real estate, and so on. Keep in mind that mutual funds and ETFs come in many different shapes and sizes. As John Bogle pointed out, the traditional index funds (TIFs) that are broad-market, low-cost, no-load index funds are designed to be bought and then held for the long term. What about derivatives — are you comfortable with them, as Myron Scholes and Robert Merton are? You may not even be aware that many investment products are actually derivatives in disguise. Your list will be the menu of assets from which the perfect portfolio will be built. Also, think about assets you aren’t willing to hold. Think about Martin Leibowitz’s dragon risks. Keep in mind, you should never make an investment based on what you think will happen if you don’t know what might happen — a lesson many learned the hard way during the financial crisis of 2007 – 2009.

6

Develop a sense of the current investment environment and how stable that environment appears to be relative to historical norms. In a stable environment, stable investment rules such as 60% stocks and 40% bonds might be sufficient, but in a rapidly changing economy, investment rules may have to be equally dynamic. The key here is to manage the risk of your perfect portfolio so you are (a) exposed to only those risks that you’re comfortable bearing (based on principles 2 and 3 above), (b) maximally diversified across investments that carry the highest possible premium relative to their risk, and (c) comfortable monitoring your investments on a regular basis, especially as market conditions and your own personal circumstances change over time.

7

Avoid obvious investing mistakes. Bogle and Charles Ellis remind us that these mistakes may include paying higher fees than needed, experiencing high (and potentially costly) turnover in your portfolio, needlessly incurring taxes, and investing with active managers based solely on trust and friendly connections. That guy Bernie may be charming on the golf course, but be careful giving him your money. If you decide to take on a lot of additional risk by borrowing to invest, make sure you’ve got the cash reserves for margin calls. Shiller reminds us that we don’t always act rationally. We may think of ourselves as Mr. Spock from “Star Trek,” but often act more like Homer Simpson.

Excerpted from the book "In Pursuit of the Perfect Portfolio" by Andrew W. Lo and Stephen R. Foerster. Copyright © 2021 by Andrew W. Lo and Stephen R. Foerster. Published by Princeton University Press. All Rights Reserved.

Read next: To build a better portfolio, account for 'shocks and drifts'