MIT Golub Center for Finance and Policy

Economics

Financing Treasury Debt with SOFR Floating Rate Notes: Is It a Good Idea?

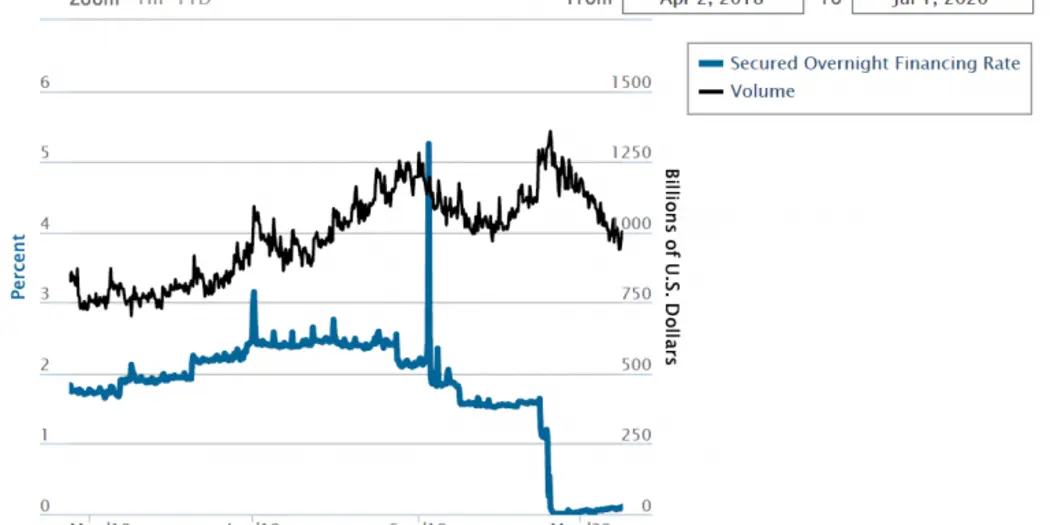

About ten years ago, the LIBOR manipulation scandal unfolded, resulting in billions of dollars in fines levied on several major banks. Since then, global regulators have embarked on a long journey to find a new reference rate to replace LIBOR. A credible and widely recognized reference rate enables market participants to easily write debt, derivatives and other financial contracts to hedge and transfer interest rate risks. Today, the leading candidate for replacing LIBOR in the U.S. is the Secured Overnight Financing Rates, or SOFR, which is calculated as a volume-weighted median rate of overnight repurchase agreements (repos) that are collateralized by U.S. Treasury securities. SOFR is published daily by the Federal Reserve Bank of New York (FRBNY) since April 2, 2018. The chart below, obtained from the FRBNY website, shows SOFR and underlying repo transaction volume from April 2, 2018 to July 1, 2020. Approximately $1 trillion of repo transactions take place daily, making SOFR a robust reference rate that is difficult to manipulate. SOFR also closely tracks other short-term interest rate such as Fed Fund rate (not shown in the chart), but it is more sensitive to funding market stress, shown in the occasional spike-ups.

The organic growth in the liquidity of SOFR market, however, has not reached a level anywhere near the liquidity of LIBOR market that SOFR is intended to replace. Trillions of dollars of debt instruments (e.g., business loans and mortgages) and hundreds of trillions of dollars of derivatives contracts (e.g., futures and swaps) are still linked to LIBOR. In contrast, as of July 2020, the CME SOFR futures are liquid only up to two years. The trading volume of SOFR swaps is also dwarfed by that of LIBOR swaps, according to Clarus Financial Technology. Private-sector issuance of SOFR FRNs has been of low volume and relatively short maturities.

Against this backdrop, the U.S. Treasury’s active consideration of issuing SOFR-linked floating rate notes (FRN) is a significant development. See the Treasury’s notice and request for information. Is issuing SOFR FRN a good idea for the U.S. Treasury?

The benefits of issuing SOFR FRNs

Let’s start with the benefits. Clearly, the issuance of SOFR FRNs by the largest issuer of U.S. dollar assets will significantly boost the liquidity of SOFR market and speed up the transition away from LIBOR. But perhaps a more important question is whether SOFR FRNs would attract strong demand and have low financing costs. There are at least two reasons that they could.

First, SOFR FRNs have stable market prices and are likely to attract money market investors. Cash flows from SOFR FRNs would be indexed to SOFR, such as SOFR plus a spread. Because each coupon payment moves in tandem with the discount rate on that coupon, the market value of an FRN stays close to its face value. This feature is highly desirable for money market mutual funds. After SEC’s money market mutual fund reform, prime money market funds must use a floating NAV, and price-stable FRNs reduce their NAV volatility. Price-stable securities could also be attractive to government money market funds that use a fixed NAV. In addition, the SEC treats the maturities of FRNs as the time until the next floating rate reset date, which relaxes some regulatory constraints faced by money market funds regarding the maturity of the securities they hold.

Evidence from the U.S. Treasury’s issuance of FRNs linked to 13-week Treasury Bills since 2014 provides useful clues to the future of SOFR FRNs. The T-Bill FRNs have proved to be popular among money market investors. For example, Fleckenstein and Longstaff (2020) show that nearly 40% of T-Bill FRNs are held by U.S. money market funds. They also show, by a replication argument, that T-Bill FRNs are priced a few basis points higher than the replicating portfolio involving Treasury Notes and Treasury Bills. The U.S. Treasury’s own analysis in 2017 also finds that T-Bill FRNs have reduced its realized interest rate expenses compared to 2-year fixed-rate Treasury Notes. Money market investors that have invested in T-Bill FRNs are likely to greet SOFR FRNs with similar enthusiasm.

In addition, money market mutual funds are active investors in the tri-party repo market. According to data from the FRBNY, the average SOFR from April 2, 2018 to June 25, 2020 is 1.789%, whereas the average tri-party repo rate in the same period is 1.767%. These rates are comparable, suggesting that money market funds’ demand for SOFR FRN would be as strong as their demand of tri-party repos.

The second benefit of SOFR FRNs is their effective hedge against funding risk. Financial intermediaries such as dealer banks are major participants in Treasury markets because Treasury securities are collateral for financing in the repo market. By purchasing Treasury securities and financing them in the repo market, an investor receives the coupon rate of the Treasury securities and pays the repo rate. For the vast majority of Treasury notes and bonds, the coupon rate is fixed, but the repo rate is time-varying. During a market stress event such as in September 2019, when SOFR settled above 5%, the financing cost can far exceed the Treasury coupon rate, making the Treasury security “expensive” to hold. The same risk applies to other leveraged investors of Treasury securities such as hedge funds.

Cash flows from SOFR FRNs are a natural hedge against fluctuations of funding costs. The funding cost of a SOFR FRN is the repo rate that a Treasury investor pays in the repo market. The cash flow from a SOFR FRN is SOFR itself, which is a median of all repo rates. There is a dispersion of repo rates in the market, so the hedge is imperfect, but it is decent one. Data from the FRBNY show that the 1st, 25th, 75th and 99th percentiles of repo rates all have a correlation of at least 0.95 with SOFR (which is the median of repo rates).

The hedging property of SOFR FRNs implies a potentially strong demand from primary dealers, hedge funds, and other investors that use the repo markets for funding Treasury securities. Although the SOFR FRN may incur a higher interest expense than standard Treasury Bills and Notes when repo rate spikes up during a market stress, this temporarily higher interest expense should be more than offset by the lower yield (average cost) on the SOFR FRN. Put differently, by issuing the SOFR FRN, the Treasury can harvest an “insurance premium” by insuring leveraged investors against funding market stress.

The risks of issuing SOFR FRNs

One obvious risk of issuing SOFR FRNs is that the SOFR market is relatively illiquid. Issuing debt into a shallow market could be expensive. For example, Fleckenstein, Longstaff, and Lustig (2014) find that Treasury TIPS tend to be significantly underpriced compared to replicating portfolios involving nominal Treasury securities (and inflation swaps) between 2004 and 2009. The underpricing is about $2 per $100 face value before the crisis of 2008-09 and about four times as large during the crisis. The authors further find that the underpricing is alleviated after hedge fund capital flows into exploiting this mispricing. A repeat of the TIPS underpricing in SOFR FRNs, even if temporary, could be costly for the U.S. Treasury.

Another risk of issuing SOFR FRNs is the potentially nonstandard discounting convention. SOFR is an overnight rate, but FRNs have cash flows far into the future. There is no “term SOFR” yet, i.e., there is no readily available SOFR-based discount rate for cash flows that happen more than one day away. The industry has not converged on the discounting convention, although compounding daily rates seems preferable to simple averages of daily rates because compounded rates best preserve price stability.

Summary

As a new way to finance U.S. Treasury debt, SOFR FRNs present opportunities and risks. Strong demands are likely to come from money market investors who value stable prices, as well as from dealers and other repo-market participants who wish to hedge their funding risks. Because SOFR is an overnight rate, SOFR FRNs have the potential to save the Treasury a fraction of the term premium while offering long-term financing. On the other hand, details matter tremendously in market design, and it’s always prudent to start in small steps and adjust the plan according to market demands. Overall, given the ballooning U.S. government debt, the time seems ripe for the U.S. Treasury to take another calculated risk, to give SOFR FRNs a try. In my view, the potential benefit for U.S. taxpayers outweighs the risks.

References

The Alternative Reference Rate Committee, 2018. Second Report. https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2018/ARRC-Second-report

Clarus Financial Technology, 2019. “SOFR Swaps and SEF Venues.” https://www.clarusft.com/sofr-swaps-and-sef-venues/

CME SOFR futures statistics. https://www.cmegroup.com/trading/interest-rates/stir/three-month-sofr_quotes_globex.html

Federal Reserve Bank of New York. Secured Overnight Financing Rate Data. https://apps.newyorkfed.org/markets/autorates/SOFR

Fleckenstein and Longstaff, 2020. “The US Treasury floating rate note puzzle: Is there a premium for mark-to-market stability?”, forthcoming in the Journal of Financial Economics. https://www.sciencedirect.com/science/article/pii/S0304405X20301215

Fleckenstein, Longstaff, and Lustig, 2014. “The TIPS‐Treasury Bond Puzzle.” Journal of Finance, 69: 2151-2197. https://onlinelibrary.wiley.com/doi/full/10.1111/jofi.12032

U.S. Treasury, 2020. “Development and Potential Issuance of Treasury Floating Rate Notes Indexed to the SOFR.” https://www.regulations.gov/document?D=TREAS-DO-2020-0007-0001